The ITAT ruled that a notice under Section 148 of the Income Tax Act, despite being dated earlier, is barred by limitation if it is signed and served beyond the prescribed period. This establishes the necessary timeliness in reassessment procedures.

ITAT Clarifies Limitations on S.148 Notices

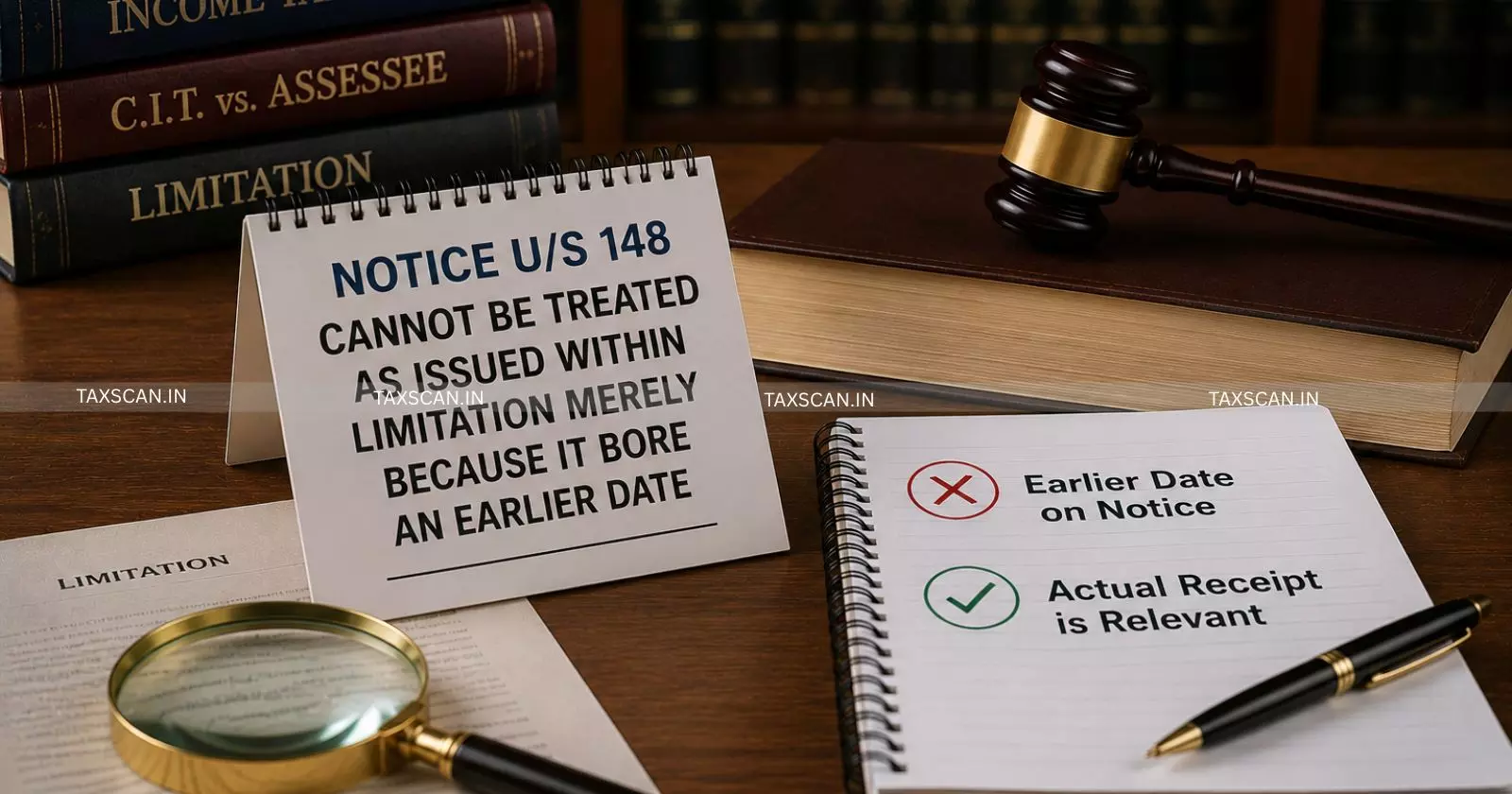

The Income Tax Appellate Tribunal (ITAT) has ruled that notices issued under Section 148 of the Income Tax Act, even if they bear an earlier date, cannot be considered valid if signed and served beyond the statutory limitation period. This decision emphasizes strict adherence to the timelines outlined by the Act.

The tribunal's decision was based on the legal requirement that reassessment proceedings must be initiated within the timeframe established by law. The court noted that the intention behind the Act is to ensure that taxpayers are given a fair notice period and that delays cannot be overlooked merely due to incorrect dating of the notice.

This ruling serves as a crucial reminder for tax practitioners to monitor the dates of notices seriously and ensure compliance with statutory limitations when representing clients in reassessment matters. Any oversight regarding timing could undermine the validity of the notice and the reassessment process.

Citations

- ITAT (2026) Tax Reporter Page